After the presidential election last November, a clear narrative took root in financial markets. A Trump presidency was supposed to result in faster policy tightening at the Fed, more growth, more inflation, and higher rates. With each new move to 2017's lowest rates, that narrative continues to unravel. This week provided a great example.

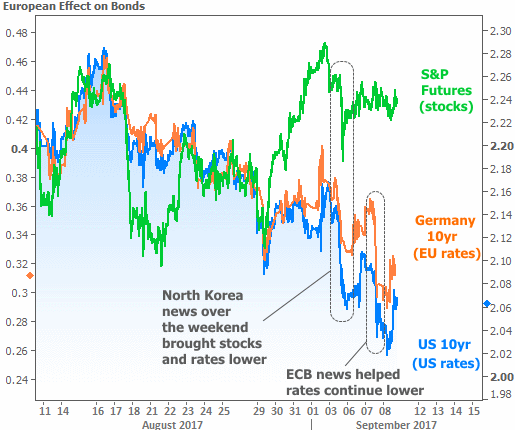

Rates began the week surging to new 2017 lows as news broke that North Korea tested what it claimed was a hydrogen bomb. Additionally, South Korea warned that another test launch was possible in the coming weeks, and Trump pledged to make "sophisticated military equipment" available for purchase by allies in the region.

In other words, it was just another weekend with looming risk of global nuclear conflict. While that's nothing new these days (sadly), it's still scary every time. Financial markets tend to process that fear by moving out of stocks and into safe-haven assets like bonds, cash, and gold. Excess investor demand for bonds results in lower rates.

Later in the week, rates continued lower as the European Central Bank released a very timid policy statement as well as a downwardly revised inflation forecast. Whether at home or abroad, the longer it takes for big central banks to unwind their bond-buying programs (bond-buying helps rates) and for inflation to pick up (inflation hurts rates), the easier it becomes for rates to stay low (or move even lower).

What makes this week's push to lower rates interesting is the fact that 2017's Trump-related narrative actually saw some support. Trump reached across the aisle and struck a deal with congressional democrats that funded disaster relief and temporarily raised the debt ceiling through the end of the year.

While this successful example of bipartisan policymaking clearly did some damage to bond markets (i.e. rates went a bit higher on Wednesday), its effects were ultimately steamrolled by the week's dominant events. In other words, investors don't suddenly see new inflation risks and growth potential due to this week's legislative efforts.

In fact, some of the biggest, savviest investors haven't been too concerned about such things for many months. Before Trump was elected, rates had generally been falling the better part of 3 years. Volatility was decreasing and it wasn't clear what it would take for things to change.

The Trump victory provided a solution for one of two reasons. For those who believed that new policies could stimulate growth and inflation, there were good reasons to push rates rapidly higher at the end of 2016. Those who didn't necessarily see fiscal policy miracles in store were still thrilled to have justification to get bond markets moving again. They saw great buying opportunities in the future based on the inflation/growth narrative.

As fiscal policy progress continues proving elusive, and as inflation has moved frustratingly lower, that pessimistic group of investors has been ringing the cash register by buying the bonds that the average investor couldn't wait to sell.

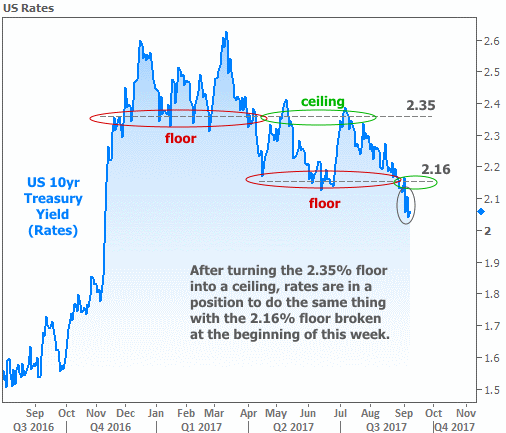

If we look at this process in terms of 10yr Treasury yields (the best benchmark for momentum in long-term rates like mortgages), we can see where some investors stepped in to buy bonds when yields hit 2.5-2.6. There was relative equilibrium around 2.35%, with sellers able to keep yields from falling much lower in the 1st quarter.

Things changed in April, with rising geopolitical tensions, fiscal policy missteps, and a more timid Federal Reserve. What had been a "floor" around 2.35% now became a ceiling, and the game between buyers and sellers resumed.

This time around, the floor was closer to 2.12%. While it didn't see bounces as frequently, the big bounce in late June was a watershed moment for global bond markets. That's when investors picked up their first major signal that the European Central Bank (ECB) might be close to winding down its bond-buying plan.

2.12% quickly became a distant memory. Whether or not the ECB was serious, investors figured those rates were too low until they could get clarification. As mentioned above, that clarification came this week and was joined by the North Korea headlines. The combination of the two events was enough to break the 2.12% floor.

Now the question becomes whether this floor will be able to act as a ceiling. It's too soon to say--especially with the Fed's hotly-anticipated policy announcement coming up in just under 2 weeks. At the very least, 2017 has proven to be much more of a friend than an enemy for fans of low rates.

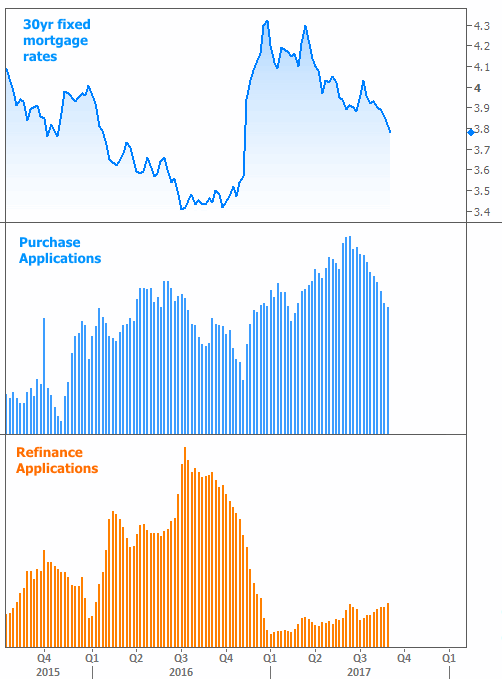

That friendliness is apparent in the mortgage market. Now that the seasonal slide in home purchase activity has set in (compounded by non--seasonal weakness due to inventory constraints), refinances are picking up the slack in mortgage applications. If rates continue lower, loans originated in the first quarter will increasingly be "in the money" when it comes to a refinancing.